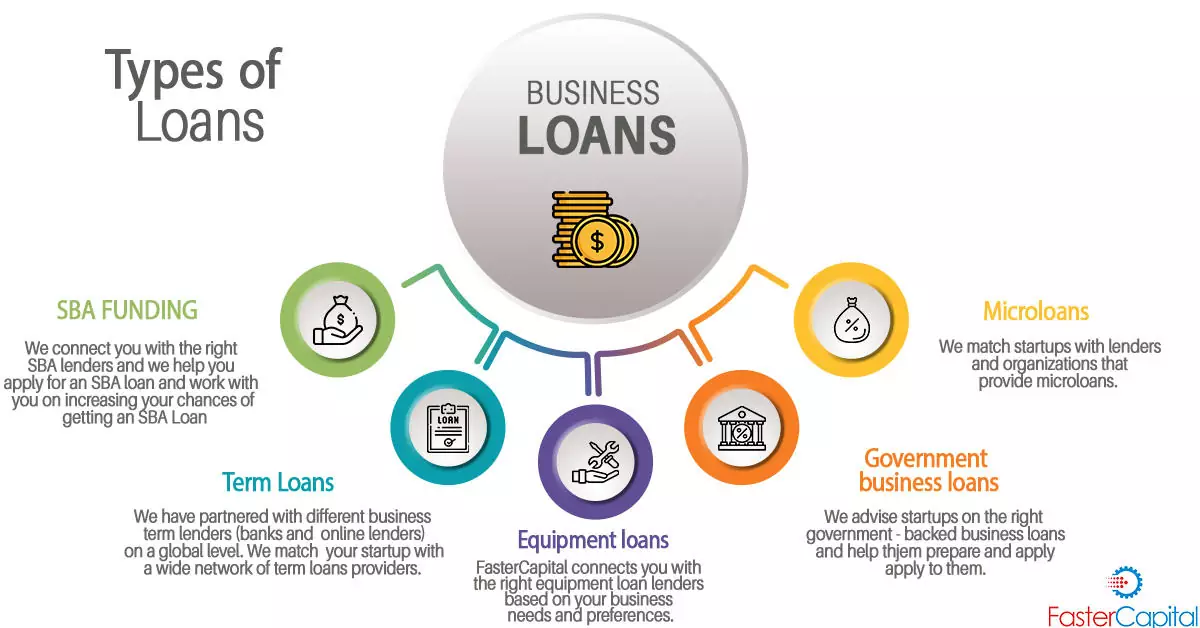

For startups, securing funding can be one of the biggest challenges. Understanding the business loan eligibility criteria is crucial for improving the chances of approval. A startup business loan can provide the necessary capital to launch operations, expand offerings, or manage initial expenses, but lenders evaluate applications carefully to mitigate risk. By preparing in advance and aligning your financials with lender expectations, your startup can increase its chances of obtaining the right financing.

Understand the Business Loan Eligibility Criteria

Lenders assess multiple factors before approving a business loan. The business loan eligibility criteria typically include the applicant’s credit score, business plan, financial stability, repayment capacity, and the legal structure of the startup. Startups often face stricter scrutiny because they have limited operational history and uncertain cash flow. By understanding these criteria, founders can prepare the necessary documents and address potential weaknesses in their applications.

Maintain a Strong Credit Profile

One of the most important factors in meeting business loan eligibility criteria is a strong credit profile. Lenders evaluate both the personal credit history of the founders and the financial history of the startup if available. Timely repayment of previous loans, responsible use of credit cards, and maintaining a good credit score signal reliability to lenders. Even a startup business loan can be easier to secure if founders demonstrate financial discipline and a trustworthy credit background.

Prepare a Detailed Business Plan

A comprehensive business plan is essential for meeting lender expectations. The business plan should clearly outline the startup’s objectives, market analysis, revenue model, funding requirements, and projected cash flows. Lenders use this plan to evaluate the feasibility and sustainability of the business. Including a repayment strategy and a timeline for achieving profitability can enhance your credibility and satisfy key aspects of the business loan eligibility criteria.

Maintain Proper Documentation

Proper documentation plays a crucial role in the approval process for a startup business loan. Lenders typically require identity and address proof, business registration documents, financial statements, bank account records, tax filings, and legal licenses. Having all these documents ready and organized not only speeds up the process but also demonstrates professionalism, which increases the likelihood of approval under the business loan eligibility criteria.

Demonstrate Repayment Capacity

Lenders want assurance that the loan will be repaid on time. A clear plan for cash flow management and revenue generation helps demonstrate repayment capacity. For startups, highlighting any secured contracts, potential clients, or early revenue can support your application. Properly projecting income and expenses shows lenders that the startup can meet the repayment obligations required by the business loan eligibility criteria.

Consider Collateral or Guarantors

Offering collateral or a guarantor can improve eligibility for a startup business loan. Secured loans reduce the lender’s risk and may result in better loan terms, including lower interest rates. Collateral can include property, equipment, or other assets. Even though some startups may prefer unsecured loans, having collateral can make a significant difference in meeting the business loan eligibility criteria.

Build a Relationship with Your Bank

Maintaining a positive relationship with a bank or financial institution can also help meet eligibility requirements. Startups with existing accounts and transaction history at a bank are often evaluated more favorably. Regular banking activity demonstrates financial stability and accountability, which are key aspects of the business loan eligibility criteria.

Final Thoughts

Meeting the business loan eligibility criteria is essential for securing a startup business loan. By maintaining a strong credit profile, preparing a detailed business plan, organizing proper documentation, demonstrating repayment capacity, and offering collateral if possible, startup founders can significantly improve their chances of approval. Understanding lender requirements and presenting a professional and transparent application helps startups access the funding needed to grow operations, achieve profitability, and establish a strong foundation for future business success.